The first half of 2022 ended with both stock and bond markets firmly in the red amid a combination of less-than-ideal macroeconomic factors. Weakness in the technology sector resulted in losses to leading indexes as investors sought to de-risk their portfolios amid numerous central bank interest rate increases and persistently elevated inflation. Volatility spiked numerous times, reversing the trend seen during the 2020 – 2021 low-interest rate environment.

With bonds falling in tandem with stocks, some traditional diversification approaches used by passive investors are failing to provide sufficient downside protection and income potential. This can be difficult for investors with defined income needs, such as retired Canadians, who rely on their portfolio’s yield to sustain a safe, perpetual withdrawal rate.

During times of elevated volatility, an active management approach, using options writing strategies, has the potential to both enhance yield and improve risk-adjusted returns. In particular, entrusting a competent fund manager with implementing covered call overlays on attractive underlying equity indices or sectors can be a great way to harness volatility while preserving upside potential.

How Covered Call Strategies Work

A call option is a derivative that gives the buyer the right, but not the obligation, to purchase 100 shares of a stock at an agreed-upon price by a certain date. See the illustration below as an example.

Options are comprised of the following mechanisms:

- Strike price: The price at which the buyer of the call option can purchase the shares.

- Premium: The price at which the buyer of the call option pays for a single call option.

- Expiration date: The latest date the buyer of the call option can choose to exercise the option and purchase 100 shares of the stock at the strike price.

Investors who can sell call options assume the obligation of delivering 100 shares of the stock to the buyer if the call is exercised before expiry. In return, the investor receives a premium. A covered call is when the investor physically holds shares of the stock and then proceeds to sell a call option for every 100 shares of that stock. In return, the investor receives a cash premium, the amount of which tends to increase when:

- The implied volatility of the stock is higher than the historical average.

- The time until the expiry of the call option is dated further out.

- The strike price of the option is “in-the-money” (below the current price of the stock) or “at-the- money” (the same as the current price of the stock).

In general, there are two outcomes for the investor who sells the covered call:

- The call expires with the stock’s price below the strike price (out-of-the-money). The investor keeps both the premium and the underlying 100 shares.

- The call expires with the stock’s price above the strike price (in-the-money). The investor keeps the premium but must sell the underlying 100 shares to the buyer of the call at the agreed-upon strike price.

In scenario #1, the investor profits from the cash premium received but is still exposed to the downside of holding the stock. If the value of that stock drops, the investor will incur an unrealized loss that can be offset somewhat by the premium received.

In scenario #2, the investor profits from the cash premium in addition to selling 100 shares of their stock to the buyer at the higher strike price. Depending on the cost basis and strike price, this can cap the investor’s potential gains if the price of the underlying stock moved sharply past the strike price.

FOR ILLUSTRATIVE PURPOSES ONLY

Why an ETF Approach to Covered Calls?

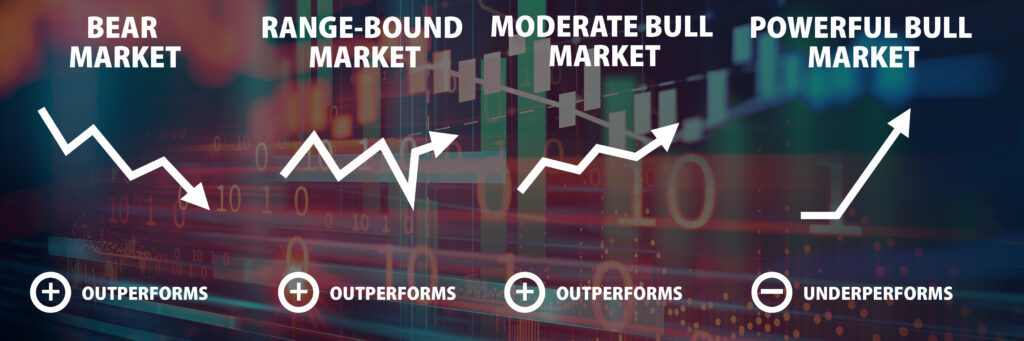

Typically, the performance of a covered call strategy versus a buy-and-hold index investing strategy depends on the underlying macroeconomic conditions. Generally, we see:

- In bear markets: Covered call strategies can outperform as the premium received can offset unrealized losses, while higher-than-average spikes in volatility (especially during bear market rallies) can typically increase options premiums.

- In range-bound markets: Markets that trade sideways generally experience high volatility, which increases the size of options premiums. In addition, stocks that trade range-bound are more likely to expire out-of-the-money, which is beneficial for covered call strategies.

- In moderate bull markets: Covered call strategies generally benefit during moderate, slightly volatile bull markets as the underlying stocks can participate in upside potential while having some income potential from options premiums.

- In powerful bull markets: Covered call strategies generally underperform as the price of the underlying stocks blows past strike prices and are called away, but some upside participation is still possible along with income earned from the premium.

The other use for a covered call strategy is as an additional diversified source of income to supplement traditional yield-generating assets, such as corporate bonds. With further interest rate hikes anticipated, rising inflation, and increasing bond yields, fixed income assets may not provide income investors with a desirable risk-return profile.

A covered call strategy can mitigate this by allowing investors to harness their equity allocation to increase yield without sacrificing room for the aforementioned alternatives. This way, investors do not necessarily have to increase their fixed income allocation to increase the level of income generated by their portfolio, thus offering a more defensive posture in a rising rate environment.

For retired investors in the withdrawal phase, a covered call strategy can potentially help to ensure a perpetual withdrawal rate by offering a sufficiently high equity allocation, while providing distributions that typically exceed those of dividend stocks. This can mitigate the need for investors to sell shares, maximizing their ability to meet income needs via options premiums.

The premiums received can also be used for income, saving investors and advisors from having to sell shares if withdrawals come in during downturns.

Finally, options premiums are also taxed favourably as capital gains, making this strategy tax efficient compared to interest income incurred from bond funds and competitive against rates on qualified Canadian dividends. For non-tax advantaged accounts, covered call strategies can provide a much more tax-efficient income stream to comparatively inefficient assets like REITs or bonds.

Why an ETF Approach to Covered Calls?

While considered relatively elementary as an option strategy, covered calls can be difficult, costly, and time-consuming for most retail investors to implement. Investors must select an appropriate portfolio of underlying securities, have sufficient capital to purchase shares in increments of 100 and possess the knowledge to select the correct strikes, and expiry dates, and watch for excessively wide bid-ask spreads.

For investors seeking to maximize their covered call strategies, a strong understanding of the Options “Greeks”, including Delta, Theta, Gamma, and Vega, along with implied versus historical volatility is necessary as well. Once the call is sold, managing the position is more complex than just collecting the premium and letting it ride. Should a position go in-the-money, the investor must determine whether to leave it be, roll the strike price up, or roll the expiry date out, lest they risk early assignment.

A much simpler and capital-efficient approach is through an exchange-traded fund (ETF) that holds a portfolio of underlying stocks with a covered call overlay. Investors who buy these ETFs benefit from the professional expertise of a fund management team, who handles the technical end of managing a covered call strategy.

In return for a management expense ratio, investors can forego having to manually execute trades and rebalance their positions, which can quickly add up in commission costs and bid-ask slippage. Difficult aspects of options trading like risk management and position sizing are eliminated in favour of a simpler buy-and-hold approach using ETFs.

The Horizons ETFs Difference

Many fund managers implement covered call strategies in a mechanical, passive fashion. For example, a common approach is writing at-the-money calls with less than two months until expiry on 100% of a portfolio’s underlying stocks.

This approach does not require strong active management and may produce high premiums, but is sub-optimal for the following reasons:

- At-the-money calls have a greater chance of becoming in-the-money and being exercised, which can cap returns for covered call writers.

- Writing calls on 100% of a portfolio’s holdings reduces upside potential significantly.

- Mechanically writing calls consistently with the same time until expiry and strike price does not consider changes in volatility, which can significantly affect premiums.

Horizons ETFs favours an active management approach. This means the fund managers have broad discretion to consider a variety of factors when it comes to selecting the best strikes and expiry dates to sell options at, including option’s delta, implied volatility, and macroeconomic factors. This dynamic approach is more flexible, tactical, and designed to capitalize on or limit the impact of different market conditions.

Writing calls systematically with at-the-money strikes and consistent expiry dates can give up a lot of upside potential and may cause investors to miss out on heightened premiums from surges in volatility. The Horizons ETFs’ active management approach enables fund managers to assess option’s deltas, harness implied volatility, and capture the most time decay (theta) for the possible best asymmetrical risk-return payoffs.

In addition, Horizons ETFs’ covered call ETFs cap covered call overlays on no more than 50% (33% in the case of HGY) of the underlying portfolio’s holdings. Compared to strategies that write calls on 100% of the underlying portfolio, Horizons ETFs’ approach is designed to preserve the upside price potential of the underlying holdings. Fund managers are also capable of targeting specific individual tickers in the underlying portfolios that are experiencing higher-than-normal volatility to maximize premiums. This makes the strategy more bullish and focused on long-term appreciation versus strictly maximizing income.

The Horizons Lineup

Horizons ETFs’ suite of covered call ETFs is designed with meaningful exposure to popular equity sectors, indices, and asset classes, like energy, gold, the NASDAQ, and the S&P/TSX 60TM Index, as an alternative to traditional index funds. With a focus on upside appreciation, the funds work to harness volatility as a way to generate supplemental income from covered call premiums.

The Horizons Covered Call ETFs, except HGY (capped at 33%), write out-of-the-money calls, generally, on no more than 50% of the underlying holdings. This approach balances upside participation to ensure the opportunity to gain attractive income potential from the covered calls, while lowering the risk of assignment and capping returns if the underlying stock experiences a strong upwards movement.

The underlying securities in Horizons ETFs’ covered call ETFs represent common core or thematic portfolio holdings suitable for a variety of investors with different risk tolerances, market outlooks, and investment objectives. While the covered call overlay is actively managed, the underlying securities are passively managed according to rules-based indexing methodologies to ensure low turnover and tracking error.

Commissions, management fees and expenses all may be associated with an investment in exchange traded products managed by Horizons ETFs Management (Canada) Inc. (the “Horizons Exchange Traded Products”). The Horizons Exchange Traded Products are not guaranteed, their values change frequently and past performance may not be repeated. The prospectus contains important detailed information about Horizons Exchange Traded Products. Please read the relevant prospectus before investing.

The investment objectives of the Horizons Canadian Large Cap Equity Covered Call ETF (“CNCC”) (formerly Horizons Enhanced Income Equity ETF (“HEX”)), Horizons Canadian Oil and Gas Equity Covered Call ETF (“ENCC”) (formerly Horizons Enhanced Income Energy ETF (“HEE”)), Horizons Equal Weight Canadian Bank Covered Call ETF (“BKCC”) (formerly Horizons Enhanced Income Financials ETF (“HEF”)), Horizons US Large Cap Equity Covered Call ETF (“USCC.U, USCC”) (formerly Horizons Enhanced Income US Equity (USD) ETF (“HEA.U, HEA”)), Horizons NASDAQ-100 Covered Call ETF (“QQCC”) (formerly Horizons Enhanced Income International Equity ETF (“HEJ”)), and the Horizons Gold Producer Equity Covered Call ETF (“GLCC”) (formerly Horizons Enhanced Income Gold Producers ETF (“HEP”)), were changed following receipt of the required unitholder and regulatory approvals. The ETFs’ new names and tickers began trading on the TSX on June 27, 2022. For more information, please refer to the disclosure documents of the ETFs on www.HorizonsETFs.com.

The financial instrument is not sponsored, promoted, sold, or supported in any other manner by Solactive AG nor does Solactive AG offer any express or implicit guarantee or assurance either with regard to the results of using the Index and/or Index trade name or the Index Price at any time or in any other respect. The Index is calculated and published by Solactive AG. Solactive AG uses its best efforts to ensure that the Index is calculated correctly. Irrespective of its obligations towards the Issuer, Solactive AG has no obligation to point out errors in the Index to third parties including but not limited to investors and/or financial intermediaries of the financial instrument. Neither publication of the Index by Solactive AG nor the licensing of the Index or Index trade name for the purpose of use in connection with the financial instrument constitutes a recommendation by Solactive AG to invest capital in said financial instrument nor does it in any way represent an assurance or opinion of Solactive AG with regard to any investment in this financial instrument.

Nasdaq®, Nasdaq-100®,and Nasdaq-100 Index®, are trademarks of The NASDAQ OMX Group, Inc.(which with its affiliates is referred to as the “Corporations”) and are licensed for use by Horizons ETFs Management (Canada) Inc. The Fund(s)have not been passed on by the Corporations as to their legality or suitability. The Fund(s) are not issued, endorsed, sold, or promoted by the Corporations. THE CORPORATIONS MAKE NO WARRANTIES AND BEAR NO LIABILITY WITH RESPECT TO THE FUND(S) or PRODUCT(S).

Certain statements may constitute a forward-looking statement, including those identified by the expression “expect” and similar expressions (including grammatical variations thereof). The forward-looking statements are not historical facts but reflect the author’s current expectations regarding future results or events. These forward-looking statements are subject to a number of risks and uncertainties that could cause actual results or events to differ materially from current expectations. These and other factors should be considered carefully and readers should not place undue reliance on such forward looking statements. These forward-looking statements are made as of the date hereof and the authors do not undertake to update any forward-looking statement that is contained herein, whether as a result of new information, future events or otherwise, unless required by applicable law.

This communication is intended for informational purposes only and does not constitute an offer to sell or the solicitation of an offer to purchase exchange traded products (the “Horizons Exchange Traded Products”) managed by Horizons ETFs Management (Canada) Inc. and is not, and should not be construed as, investment, tax, legal or accounting advice, and should not be relied upon in that regard. Individuals should seek the advice of professionals, as appropriate, regarding any particular investment. Investors should consult their professional advisors prior to implementing any changes to their investment strategies. These investments may not be suitable to the circumstances of an investor.

All comments, opinions and views expressed are generally based on information available as of the date of publication and should not be considered as advice to purchase or to sell mentioned securities. Before making any investment decision, please consult your investment advisor or advisors.